Generation wealth building represents the deliberate process of creating and preserving financial assets that span multiple generations beyond your lifetime. This systematic approach to generation wealth building concentrates on developing sustainable income streams and appreciating assets that directly benefit your children, grandchildren, and future descendants. According to an article in Investopedia by Kristina Byas, titled “The Surprising Truth About Which Generation’s Wealth Is Growing the Fastest,” from 2019 to 2024, there was a $12 trillion increase in Millennials’ net worth, demonstrating the accelerating momentum of generation wealth building across family lines. In Canada alone, approximately $1 trillion in generation wealth building assets will transfer between 2023-2026. However, successful generation wealth building demands decades of disciplined saving, strategic investing, and comprehensive tax planning rather than quick fixes. Essential generation wealth building vehicles include real estate holdings, retirement accounts, trust funds, family businesses, and permanent life insurance policies that secure multi-generational financial stability. The primary objective of generation wealth building is establishing financial foundations that provide the next generation with substantial advantages rather than requiring them to build from zero. With guidance from IBC Financials’ tax advisors, you can develop a comprehensive generation wealth building strategy that positions your family generations ahead financially.

Generation wealth building encompasses the systematic accumulation and preservation of assets specifically designed for multi-generational transfer and continuation. This generation wealth building process includes diverse holdings: real estate properties, stock and bond portfolios, retirement accounts, and operating businesses that appreciate over time. As per the DFPI Canada.gov article titled “Five Steps to Building Generational Wealth,” the core principle of generation wealth building involves creating financial security that extends far beyond your own lifetime to directly benefit your heirs. Rather than merely addressing immediate expenses, generation wealth building prioritizes long-term financial security and asset preservation strategies. This generation wealth building approach provides children and grandchildren the ability to pursue opportunities with reduced financial stress, access superior education and career paths, and avoid the debt cycles that limit economic mobility for families without inherited assets.

Effective generation wealth building requires thoughtful planning and disciplined investment management throughout your lifetime to ensure sustainable wealth transfer. Working with IBC’s financial professionals simplifies the generation wealth building planning process and helps establish sustainable strategies for multi-generational prosperity.

The capital required for successful generation wealth building cannot be defined by a single threshold—it varies significantly based on family lifestyle, geographic location, ongoing expenses, and long-term objectives for wealth preservation. According to Srivindhya Kolluru’s article in Financial Post, titled “How much money do you need to have generational wealth?” in Canada, leaving more than $1.5 million per child typically represents sufficient generation wealth building to create meaningful financial impact across generations. For establishing generation wealth building that sustains multiple generations, there’s no universal magic number that guarantees success. For some families practicing disciplined financial management, a carefully invested generation wealth building portfolio of $2-3 million can sustain multiple generations effectively. For families with more expensive lifestyles or larger family structures, successful generation wealth building might require $10 million or substantially more in accumulated assets. What truly determines success in generation wealth building is asset management strategy and preservation techniques rather than just the initial dollar amount. Smart investments, properly structured trusts, disciplined expense management, and tax-efficient wealth transfer planning prove equally critical for sustainable generation wealth building. A moderately sized fortune managed with expertise and prudence can outlast a much larger inheritance that’s poorly structured or rapidly depleted by subsequent generations.

To establish generation wealth building in Canada, start by acquiring real estate property and establishing diversified investment portfolios across stock and bond markets with long-term growth potential. Successful generation wealth building in Canada requires consistent legacy planning, including registered account optimization and comprehensive estate strategies that protect accumulated assets. According to Canada Life, in the article titled “How to build generational wealth,” developing your own financial literacy forms the crucial foundation for effective generation wealth building and multi-generational prosperity. Essential strategies for Canadian generation wealth building include maximizing contributions to registered accounts (RRSPs, TFSAs, RESPs), implementing comprehensive estate planning with professional guidance, and securing appropriate life insurance coverage for wealth transfer protection. IBC Financial provides expert guidance to help you strategically plan your estate and implement generation wealth building strategies that benefit future generations with proper tax efficiency and asset protection.

Generation wealth building typically requires multiple decades of consistent effort, disciplined saving, and compound investment growth to create substantial transferable assets. The timeframe for achieving successful generation wealth building varies considerably based on starting capital, income levels, investment returns, and wealth accumulation strategies employed throughout the process. According to Robert Daugherty, in a Forbes article titled “3 Powerful Strategies For Building Multigenerational Wealth,” the fundamental principle of generation wealth building is spending considerably less than you earn while investing the difference strategically.

Here are fundamental approaches for generation wealth building:

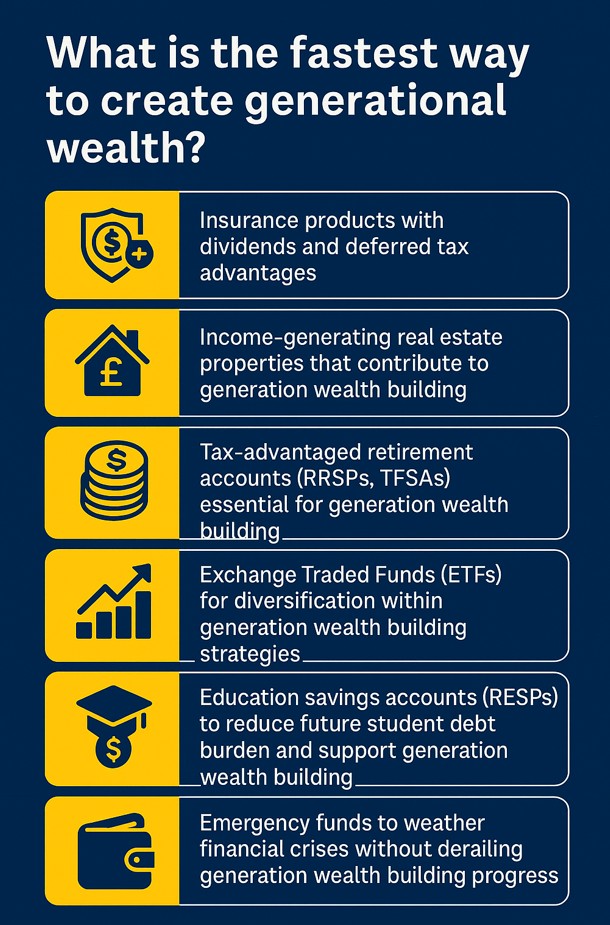

The fastest approach to generation wealth building involves amplifying passive income streams and beginning investment strategies as early as possible during your highest earning years. The most accelerated path to generation wealth building involves investing substantial portions of high salaries into diversified yet high-potential assets that appreciate over time. As per Jennifer Taylor’s NASDAQ article “10 Ways To Turn Your Six-Figure Salary Into Generational Wealth,” successful generation wealth building requires a comprehensive long-term plan with clear milestones.

For accelerated generation wealth building, prioritize substantial investments in:

To create a personalized financial and estate plan for building generational wealth, contact IBC Financial experts now. Professional financial advice accelerates your wealth building journey and helps avoid costly mistakes.

Effective approaches to generation wealth building include comprehensive estate planning, strategic tax optimization, diversified investment decisions, and properly structured trusts that preserve assets across generations. According to Scotia Wealth Management’s article “Six ways to grow your wealth tax-free in Canada,” Canadians pursuing generation wealth building should prioritize tax optimization through vehicles like tax-free savings accounts (TFSAs) and other registered plans to maximize efficiency.

Estate Planning – Estate planning forms the foundation of generation wealth building by determining how your accumulated assets, real estate holdings, and financial accounts transfer effectively when you pass away. Without proper estate planning, generation wealth building efforts face unnecessary stress, tax burdens, and often government decisions override family preferences—undermining your accumulated wealth.

Trust Structures – Trusts function as protected vehicles for your assets in generation wealth building strategies, allowing you to establish specific rules governing asset distribution. You determine who receives what assets, when distributions occur, and under what conditions for optimal generation wealth building outcomes. Many parents implementing generation wealth building use trusts to ensure children receive assets responsibly rather than dissipating wealth quickly, while also providing significant tax planning advantages. In Canada, trusts can help minimize the capital gains tax triggered by the deemed disposition of assets at death, facilitating a more efficient and controlled transfer of wealth to the next generation.

Gift Strategies – Strategic gifting during your lifetime can be highly effective for generation wealth building progress and family financial security. Whether providing down payment assistance for home purchases or transferring appreciating assets before death, gifting allows you to witness the positive impact of your generation wealth building efforts. Additionally, lifetime gifting can simplify eventual estate settlement and reduce tax burdens on generation wealth building transfers.

Tax Optimization – Without careful planning, taxes significantly erode generation wealth building efforts and reduce transferable assets to future generations. For Canadians pursuing generation wealth building, maximizing contributions to FHSAs, RRSPs, and TFSAs is essential, along with strategic investment vehicle selection that minimizes tax drag on accumulated wealth. Effective tax optimization supports generation wealth building by intelligently using available legal strategies to preserve more wealth for future generations.

Charitable Giving to Nonprofit Organizations – Charitable contributions to nonprofit organizations serve dual purposes in generation wealth building—they support causes you value while providing tax benefits that preserve more wealth for family transfer. Donations often generate significant tax deductions, and philanthropic legacies represent another dimension of generation wealth building beyond purely financial inheritance.

Generational wealth transfer occurs when parents, grandparents, or other family members pass accumulated money, property, and assets to younger generations as the culmination of successful generation wealth building efforts. This transfer represents the ultimate goal of generation wealth building—moving the older generation’s accumulated assets to family members who continue building upon that foundation for future generations. According to Thi Tran’s blog for Vancity, “Transferring generational wealth: Balancing financial and family preparedness,” Canadian history is witnessing an unprecedented generation wealth building transfer in current times.

This historic wealth transfer stems primarily from Baby Boomers benefiting from a 40-year rally in housing markets, stocks, and bonds—their generation wealth building success created substantial assets now transferring to subsequent generations. Instead of each generation starting financial journeys from nothing, successful generation wealth building and transfer provides head starts through home down payment assistance, education funding, business capital, or simply enhanced financial security and opportunity access.

No fixed dollar threshold defines successful generation wealth building—the determination depends entirely on family circumstances, lifestyle requirements, and long-term objectives for wealth preservation. Successful generation wealth building provides inheritances that meaningfully impact housing accessibility, ongoing financial support, and financial education opportunities for multiple generations. As per the CIBC report “Gifting for down payments — an update” by Benjamin Tal, for instance, the average home purchase gift in Canada now amounts to $115,000, representing one tangible measure of generation wealth building transfer in action. However, what constitutes adequate generation wealth building depends heavily on individual family needs and spending patterns across generations. The critical question for generation wealth building success isn’t the absolute dollar amount but whether accumulated money and assets can genuinely support future generations throughout their lifetimes—not just provide temporary assistance but create lasting financial advantages and reduced economic stress.

Generation wealth building integrates fundamentally into estate planning through the strategic decisions families make about asset distribution and preservation after death. Successful generation wealth building requires estate planning that pre-accounts for transfer-on-death designations, beneficiary arrangements, and tax-efficient wealth transfer mechanisms that protect accumulated assets. As per Marie-Claude Marsolais for Sun Life Canada, in the article “How to make your money last for generations,” careful estate and tax planning forms the backbone of sustainable generation wealth building strategies.

Estate planning ensures accumulated savings, property holdings, and investment portfolios from generation wealth building receive proper protection and transfer efficiently to intended beneficiaries. By planning proactively with professionally drafted wills and strategically structured family trusts, families preserve more generation wealth building assets over time while minimizing tax erosion and legal complications. Planning with IBC Financial literacy programs equips not just you, but your future generations with the knowledge to maintain and grow inherited wealth from generation wealth building responsibly.

Investments effective for generation wealth building typically begin with real estate property that appreciates over decades while potentially generating rental income for ongoing wealth accumulation. Diversified portfolios for generation wealth building include permanent life insurance with cash value accumulation, mutual funds providing broad market exposure, and various registered accounts that support long-term growth. As per BPO Canada’s article “What is generational wealth? And how to build it,” Canadians pursuing generation wealth building should utilize non-registered investment accounts, RESPs, RRSPs, FHSAs, and TFSAs strategically to maximize long-term wealth preservation potential.

Family business ownership along with stock and bond portfolios create substantial long-term value for generation wealth building strategies that span multiple decades. The essential principle involves selecting assets that appreciate consistently over time and transfer effectively to subsequent generations—providing your children and grandchildren with both stronger financial foundations and the financial literacy to continue generation wealth building across multiple generations.

You transfer generation wealth building assets by establishing clear ownership and distribution mechanisms for accumulated money, property, and investment portfolios through proper legal structures. For effective generation wealth building transfer, you create properly executed wills or trust structures ensuring assets reach intended beneficiaries according to your wishes and family objectives. As per the Investopedia article by Stephanie Powers, “Passing an Inheritance to Children: What You Must Do First,” Canadians pursuing generation wealth building must carefully consider potential inheritance taxes and capital gains implications that can significantly erode accumulated wealth if not properly planned.

Many families pursuing generational wealth building utilize permanent life insurance policies providing tax-free death benefits, or make strategic lifetime gifts that reduce eventual estate tax burdens on transferred assets. In Canada, while there is no formal estate tax, the deemed disposition rules at death can trigger significant capital gains taxes, making early planning essential. The key to successful generational wealth transfer is beginning planning early in your wealth accumulation journey, ensuring the transition proceeds smoothly without legal complications, family conflicts, or unnecessary tax erosion that diminishes what you’ve built.

To help your children successfully continue generation wealth building practices, you must actively teach them the principles and practices that created your family’s prosperity and wealth accumulation success. Helping children preserve and transfer wealth to subsequent generations requires educating them about saving disciplines, investment strategies, risk management, and long-term financial planning essential for ongoing generation wealth building. According to Royal Bank Canada’s article by Sonya Bell, titled “Investing in Your Legacy: 5 Ways to Build Wealth for Your Family’s Future,” creating lasting legacies involves imparting values and financial wisdom alongside material wealth from generation wealth building efforts.

Actively involve children in family financial planning discussions, establish irrevocable trusts where appropriate, and teach sound principles about risk tolerance and investment diversification essential for successful generation wealth building continuation. Tools like family trusts and joint ownership arrangements facilitate smoother wealth transfer while providing practical learning opportunities in generation wealth building principles. When children develop strong financial habits early through active participation in generation wealth building strategies, they’re positioned to protect inherited assets and successfully continue wealth accumulation for their own children.

Generation wealth building assets transfer after death typically through properly executed wills, trust arrangements, or other formal estate planning documents that protect accumulated wealth from unnecessary taxation. When no formal structures exist, generation wealth building transfer defaults to government-determined intestacy rules that may not reflect family wishes and often result in higher tax burdens on accumulated assets. According to Andrew Raven’s article for CPA Canada, titled “Are young people prepared for Canada’s great wealth transfer?”, families pursuing generation wealth building should seek professional guidance from tax experts to optimize wealth transfer strategies. Without proper planning, beneficiaries may face substantial capital gains taxes when generation wealth building assets are sold, significantly eroding accumulated wealth over generations. A comprehensive generation wealth building and transfer plan reduces confusion, minimizes inheritance tax exposure, and helps families preserve more accumulated wealth across generations rather than losing substantial portions to avoidable taxes and legal complications.

Yes, Infinite Banking strategies can effectively support generation wealth building through specially designed whole life insurance policies that provide tax-free death benefits to beneficiaries while allowing cash value accumulation across generations. This approach to generation wealth building allows policyholders to borrow against accumulated cash value during their lifetime for various purposes while preserving the full death benefit for wealth transfer to heirs, though this method typically involves higher costs and lower returns compared to direct investment alternatives within generation wealth building strategies. Infinite Banking for generation wealth building works best as one component within a broader, diversified estate planning strategy rather than as a standalone wealth accumulation solution. This generation wealth building approach requires consistent long-term premium payments and benefits families who prioritize guaranteed death benefits and tax advantages for wealth transfer over maximum investment growth potential.

For creating a successful generation wealth building portfolio, you must develop a comprehensive legacy plan today that incorporates multiple wealth accumulation strategies. With expert financial education and professional guidance from IBC Financial, you can ensure all aspects of your generation wealth building and transfer strategy are properly addressed. Contact us now for specialized taxation advice and comprehensive financial planning to maximize your generation wealth building success.

Take the First Step to Financial Freedom!

We use cookies for analytics & functionality. Manage preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and Privacy Policy.