The money multiplier is the ratio of the money supply to the monetary base. It shows how much of the total currency is in circulation. It is simply the reciprocal of the legal reserve ratio. This is the fraction of deposits kept in liquid assets. This ratio is used to control the amount of money in circulation. However, this practice has been abandoned by many countries. Now, central banks use policies that target inflation directly. Our experts at IBC Financial will explain this concept in detail here.

The money multiplier is the ratio of money in circulation to base money. The money multiplier shows how many times an increase in the reserves increases the money for the public. According to John Smithin’s paper “The Money Multiplier” on Academia, a one- dollar increase in base money results in more than one additional dollar increase in money in circulation.

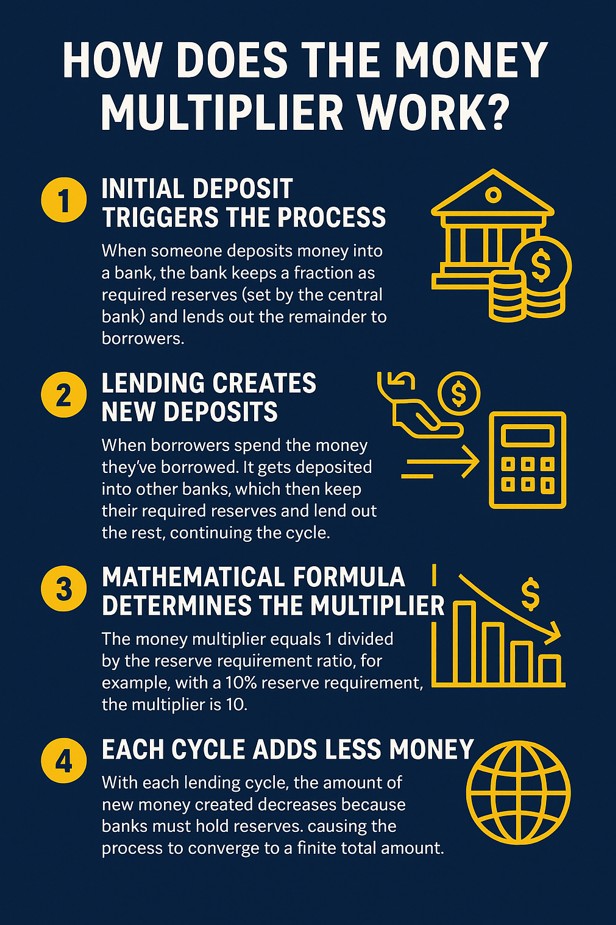

The money multiplier works by amplifying the initial deposit into a banking system through repeated cycles of lending and re-depositing, creating a larger total money supply than the original amount deposited. Here is a list of steps to explain how the money multiplier works.

According to standard economics textbooks and Federal Reserve educational materials, the money multiplier concept is fundamental to understanding fractional reserve banking and monetary policy transmission.

The money multiplier calculation is based on the level of money supply in context. Here is the formula to calculate money multiplier using a basic formula:

Simple Calculation

Money Multiplier = 1 / Reserve Ratio

For more complex scenarios, additional factors can be considered:

M1 money multiplier Calculation

M1 = 1 + (C/D) / [rr + (ER/D) + (C/D)]

C = Currency in circulation,

D = Deposits,

rr = Required reserve ratio,

ER = Excess reserves

M2 money multiplier Calculation

M2 = 1 + (C/D) + (T/D) + (MMF/D) / [rr + (ER/D) + (C/D)]

T = Time and savings deposits

MMF = Money market funds

Use the simple calculator >>

The money multiplier formula differs depending on the context. The money multiplier formula, in its basic form, is the inverse of the reserve ratio. According to Paul Krugman’s book titled “Macroeconomics” on Open Library, the simplified formula assumes that the public keeps money only in banks.

Here are the formulas

M = 1/R

R= Reserve Requirement Ratio

Or

M = Change in Money Supply/ Change in Monetary Base

Money Supply is the total amount of cash and its equivalence circulating in the economy at a given time. This includes physical cash and checkable deposits.

Monetary base is the entire quantity of money produced by the central bank. It includes the currency in circulation, bank account balances, and reserves in the central bank. It is also called high-powered money.

The monetary multiplier is inversely proportional to the reserve ratio. The monetary multiplier increases as the ratio decreases. The larger the reserve requirement, the lower the multiplier.

The money multiplier is important in macroeconomics because it regulates the money supply. Money multiplier enhances the effectiveness of monetary policies. From Adam Hayes’ article “Deposit Multiplier vs. Money Multiplier: What’s the Difference?” on Investopedia, the multiplier determines money supply.

There are a few limitations of the money multiplier, including low demand for loans. The limitations of the money multiplier make the actual value smaller. According to the article “The Limitations Of The Money Multiplier” on Faster Capital, behavioural patterns limit the money multiplier.

From our study at IBC Financial, here are four limitations of money multiplier:

The money multiplier determines the money supply. The money multiplier estimates how much the money supply will increase with an increase in the base money. According to Joachim Ahrensdorf’s paper titled “Variations in the Money Multiplier and Their Implications for Central Banking” on IMF, central banks control money supply through the monetary liabilities.

Banks play a vital role in the multiplier effect by ensuring money creation. The banks give out loans to ensure money supply. According to Akhilesh Ganti’s article “What Is the Multiplier Effect? Formula and Example” on Investopedia, banks lend one minus the reserve ratio of deposits to create money.

In the United States, the Federal Reserve influences the money multiplier through monetary policies. In Canada, the Bank of Canada fulfills a similar role by using various policy tools to manage the money supply. According to Mark Bonham’s article “Bank of Canada” in The Canadian Encyclopedia, the Bank of Canada uses various tools to influence the money multiplier.

Take the First Step to Financial Freedom!

We use cookies for analytics & functionality. Manage preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and Privacy Policy.