Tax-deferred growth is one of those quiet financial advantages that makes a huge difference in earnings over time. Tax-deferred growth is about allowing your investments to grow without paying taxes on them every single year. As per Thomson Reuters Canada on “Tax Deferral,” for Canadians, this idea is at the heart of how certain accounts like RRSPs and annuities work.

So the taxes come later, often when you’re in retirement and possibly in a lower tax bracket. Instead of paying tax every time your money earns interest or capital gain, you let it all compound. The goal is simple: keep more of your money invested for longer.

That way, it can grow faster. And as Canada’s tax-to-GDP ratio reached 34.8% in 2023, it’s a requirement. With IBC Financials’ experts helping you along the way, you can secure your family’s future. Read ahead to know all about tax-deferred growth and how it can help grow your wealth.

Tax-deferred growth means that the investment earnings are not taxed when they’re earned. Tax-deferred growth applies to earnings such as interest or dividends capital gains. As per Julia Kagan in the Investopedia article “Tax Deferred: Earnings With Taxes Delayed Until Liquidation,” you pay those taxes only later, usually when you withdraw the funds.

In a simple sense, it’s like putting your money in a “no-tax-zone” until you’re ready to use it. The common tax-deferred investments keep growing inside the account. And all that growth stays untouched by annual taxation.

Let’s say you invest $10,000 in a tax-deferred account and it grows by 5% a year. In a regular taxable account, you’d owe tax each year on that 5% as per your tax bracket. But with tax deferral, your full tax return keeps compounding.

So over many years, that difference due to lack of premature tax can be significant. Sometimes it can amount to thousands of dollars more staying in your pocket. As per IBC Financial, this delayed taxation gives your savings a long runway to build momentum. That, too, pre-tax basis, before the government takes its share.

Tax deferral works by postponing the moment when you have to pay tax on income or capital gain. Tax deferral works as a timing advantage, not an exemption. According to the Wikipedia page on “Tax Deferral,” you’ll still pay taxes eventually, but you choose when.

Here’s how it functions in practical terms:

Businesses in Canada can also benefit from deferral. For example, incorporating can allow owners to defer tax liability by leaving profits inside the company. These are also taxed at a lower corporate rate until withdrawn as dividends or salary.

There are also special salary deferral qualified plans for certain employees. And this tax-qualified defined contribution account or plan is governed by the Canada Revenue Agency. Ultimately, that allows income to be paid and taxed in a later year.

Deferral doesn’t eliminate taxes, though; it simply delays them. But this delay lets your employer dollar work harder and grow more effectively in the meantime.

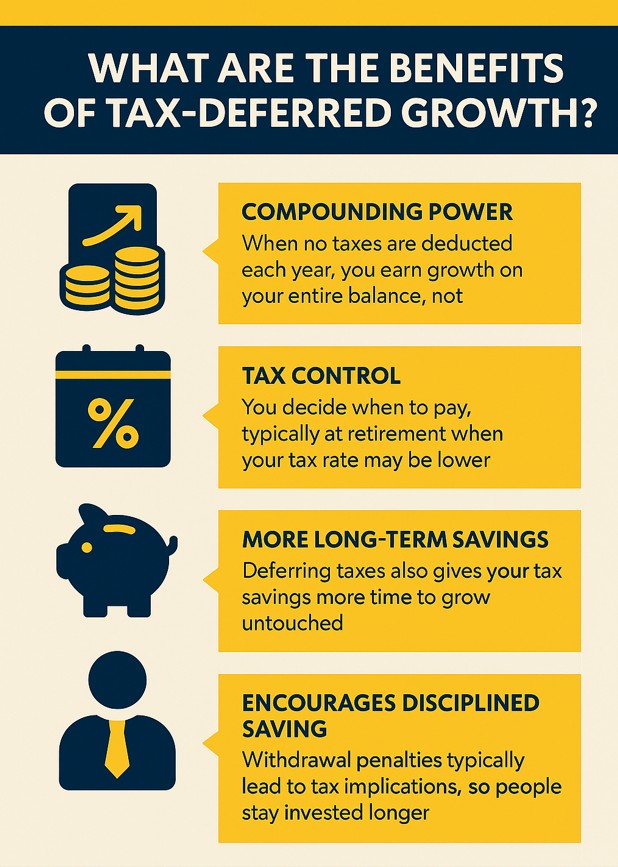

The major benefit of tax-deferred growth is compounding without interruption. Benefits of tax deferred growth include every dollar that would have gone to taxes, but stays invested and earns returns. According to the Canadian Securities Administrators, on “Types of Savings Plans,” over the years, this can lead to much larger account balances as per a third-party administrator.

Main advantages include:

Examples of earnings: Say two people invest the same amount and earn the same rate of return. Here, the one using a tax-deferred account usually ends up with a noticeably higher balance. Often, after 20 or 30 years with minimum distribution.

Accounts with tax-deferred growth in Canada include registered plans and investment products. Accounts that have tax-deferred growth include RRSPs, deferred annuities, and more. As per the Government of Canada on “RRSPs and Other Registered Plans for Retirement,” these help with your retirement plan and are designed specifically to offer tax-deferred potential growth.

Each such account serves a slightly different purpose. But they all share the same core feature: your growth of earnings isn’t taxed until withdrawn.

Common examples include:

It’s worth noting that Tax-Free Savings Accounts(TFSAs) are not tax-deferred but tax-exempt. That way, you don’t get tax deductions on the contribution limit. Nevertheless, your growth of earnings is completely tax-free, unlike in a nonqualified plan.

An IBC Financial tax professional can help you pick the best-suited accounts for your purpose. And with the right knowledge, planning, and execution in motion, you can “be your own banker.”

Tax-deferred growth in an annuity allows growth till you begin receiving payments. Tax-deferred growth in an annuity, during the accumulation phase, earns returns that aren’t taxed each year.

As per Julia Kagan and David Kindness in the Investopedia article on “Understanding Deferred Annuities: Types and How They Work for Your Future Income,” once you start drawing ordinary income, a portion of each payment represents taxable earnings. Whereas the rest, your original tax-deferred vehicle, is usually returned tax-free.

This structure allows investor benefits like catch-up contribution and postponed taxes. Along with that, there’s better post-tax income. Moreover, many people use deferred annuities as a complement to RRSPs. Particularly if they’ve already maximized their annual RRSP contribution amounts.

It also provides matching provisions for long-term, tax-free growth on a cost basis. Along with that, a predictable stream of future income, as per IBC Financial tax experts.

The difference between tax-deferred and taxable growth comes down to when you pay the tax. The difference between tax-deferred and taxable growth is that the latter gives slower growth. As per Arthur Pinkasovitch of Investopedia in “Tax-Deferred vs. Tax-Exempt Retirement Accounts,” in tax-deferred accounts, you don’t pay tax each year on the investment income. Ultimately, the full amount of tax liability keeps compounding until you withdraw.

Nonetheless, in taxable income accounts, you pay tax annually on interest, dividends, or capital gain. And these as paid as they’re earned, for instance, on money market equivalents.

Here’s a simple comparison:

| Type of Account | When You Pay Tax | Growth Impact | Typical Canadian Example |

| Tax-Deferred | Upon withdrawal | Faster growth due to compounding | RRSP, Deferred Annuity |

| Taxable | Every year on earnings | Slower growth, as taxes reduce returns annually | Regular, fixed-rate options or investment accounts |

This difference matters because paying taxes later gives your savings more time to grow. Over decades, the gap between a taxable and a tax-deferred account can be pretty substantial.

Some retirement-related accounts are not tax-deferred. Individual retirement accounts that are not tax-deferred include the Canadian Tax-Free Savings Account. As per Canada.ca, on “If you have to pay tax on a TFSA,” this account is specifically meant to grow tax-free and not deferred.

In a TFSA, contributions are made with after-tax dollars, so there’s no deduction up front. But the key advantage is that all growth and withdrawals are tax-free, forever. It’s different from tax deferral, because you never owe tax again on the gains.

Other non-deferred examples include ordinary investment or savings accounts. That’s where interest and dividends are taxed each year. Please note that tax-deferred accounts like RRSPs focus on delaying tax. On the flip side, TFSAs focus on eliminating tax on the earnings altogether.

Many Canadians use both to balance flexibility and efficiency. And we at IBC Financial recommend that, if your situation allows. Get in touch with our experts now for customized legacy and estate planning. Our taxation experts will help you grow your wealth and plan your retirement securely.

Take the First Step to Financial Freedom!

We use cookies for analytics & functionality. Manage preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and Privacy Policy.